Everyone has seen a credit card, but you might not realize that every single credit card in the world shares almost the same size, whether it is in US, EU, or China. Do you know why?

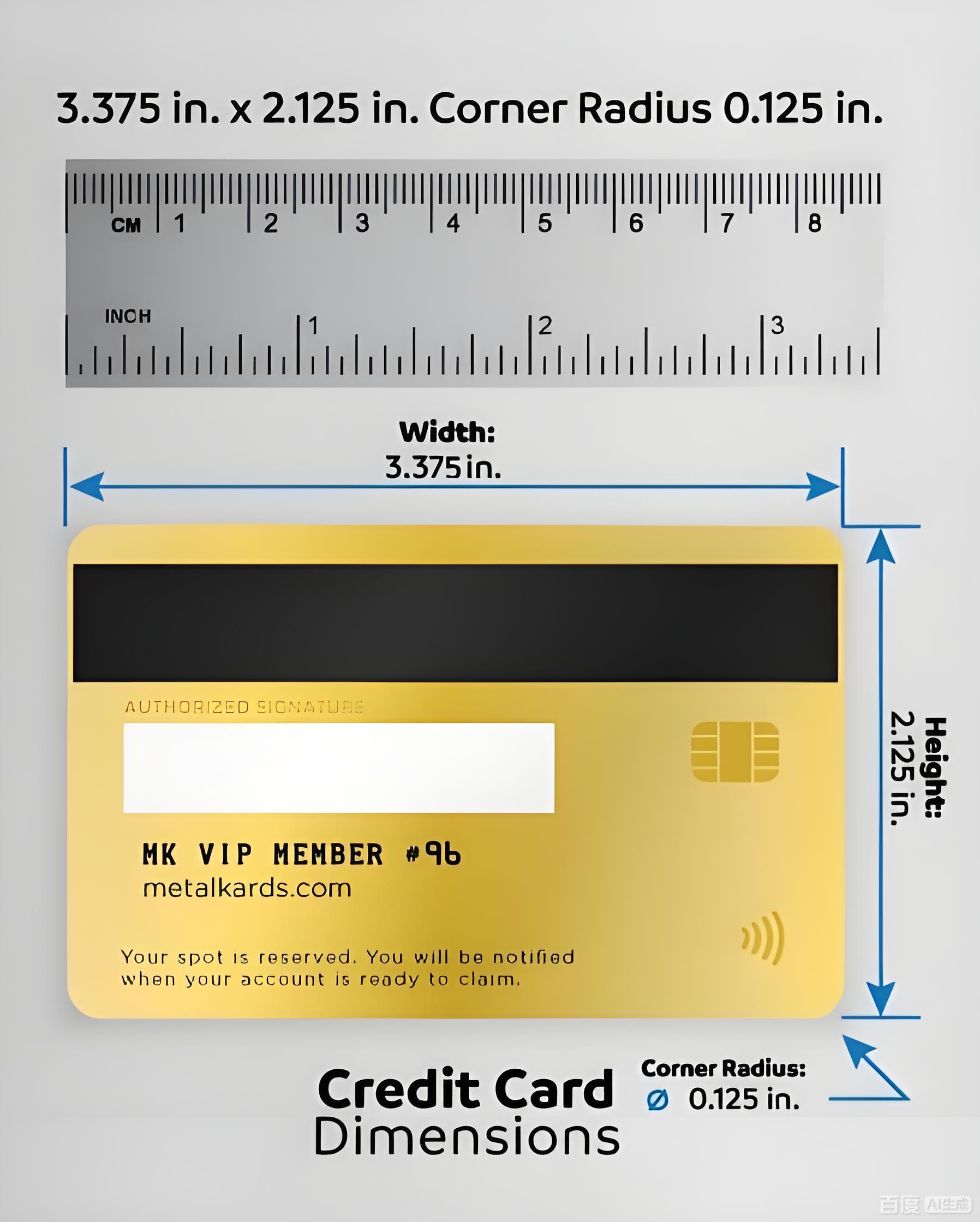

Credit Card Size table – Dimensions in inches, cm, mm, and pixels

Credit card sizes aren’t arbitrary; they follow a global standard. The specific values in different units are easy to understand when organized in a table:

| Dimension | Inches | cm | mm | Pixel (300dpi) |

| Length | 3.375 | 8.56 | 85.6 | 1012 |

| Width | 2.125 | 5.4 | 54 | 637 |

| Thickness | Approx. 0.03 | Approx. 0.076 | Approx. 0.76 | - |

Note: Pixel size is calculated based on a printing resolution of 300 pixels per inch, only for the card’s flat dimensions—there is no corresponding pixel value for thickness.

Layout of A Standard Sized Credit Card

Origin of the Size: From Chaos to Global Uniformity

How did this standard size come about? Back in the 1950s, when credit cards first emerged in the United States, they came in all shapes and sizes. Some were as big as postcards, others were narrow and short, forcing merchants to keep multiple card readers at the checkout counter — it was a real hassle.

This changed in 1959 when Bank of America launched BankAmericard (which later evolved into Visa in 1976). They had a clever idea: reference the size of cigarette packs, which were extremely popular at the time. Back then, many men kept cigarette packs in their pockets, so making cards the same size made them easy to carry, and merchants didn’t have to switch between devices. Later, in 1985, the International Organization for Standardization (ISO) officially established the ISO/IEC 7810 standard, fixing this size once and for all. Since then, credit cards have worked seamlessly with POS machines worldwide.

Regional Differences: Small Features Under Uniformity

While the size is standardized, credit cards still have subtle differences across regions.

North America is the birthplace of credit cards, and it is dominated by Visa and Mastercard. Cards here almost strictly adhere to the standard — they take these “rules” very seriously. In Europe, chip-and-PIN cards are more popular. The size remains the same, but the chip inside is slightly thicker than a magnetic stripe card — though you can’t feel the difference by touch, and it doesn’t affect usage.

In Asia, Japan and South Korea once popularized mini credit cards, roughly two-thirds the size of standard cards, designed for people who like compact items. However, they later switched back to the standard size because the mini versions were inconvenient to insert into ATMs. China’s credit cards are relative “latecomers,” but they adopted international standards from the start. Any credit card you pick up on the street will be the same size as those in New York or London.

Materials: From Fragile Paper to Premium Metal

The materials used to make credit cards have changed dramatically over the decades.

The first credit card, launched by Diners Club in the United States in 1950, was made of paper. It was soft and fragile, tearing easily if not handled carefully. By the late 1950s, PVC plastic became the new material. It’s durable and waterproof, quickly becoming the mainstream—and many basic credit cards still use it today.

Later, as environmental concerns grew, PETG material was introduced. It’s more flexible and biodegradable, and now widely used for cards in Europe. High-end credit cards take things a step further: some are made of metals like titanium alloy or stainless steel, feeling heavy and luxurious in the hand; others incorporate carbon fiber, which is lightweight yet strong, blending technology and luxury perfectly.

Functional Evolution: Same Size, Upgraded Core

While the size of credit cards has barely changed over the years, their “core” functionality has kept evolving.

Early cards only had a magnetic stripe, which stored basic account information. Swiping them made a “zizz” sound, and they were easy to clone. After 2000, chips were added. EMV chips offer far better encryption than magnetic stripes, and now most regions worldwide mandate chip-and-PIN transactions.

In recent years, virtual credit cards have emerged. They have no physical form, residing instead in mobile wallet apps as a string of numbers and a QR code. Paying with your phone is even more convenient than using a physical card. That said, many people still prefer carrying physical cards—there’s a reassuring feeling when you touch the cool plastic (or metal) and sign after swiping that virtual cards just can’t replicate.

Credit Card vs. Debit Card

Credit card and debit card are nearly identical in size and material.

Size-wise, both follow the ISO/IEC 7810 standard: 3.375 inches (85.6mm) long, 2.125 inches (54mm) wide, and about 0.03 inches (0.76mm) thick. Their printing pixel size (1012×637 at 300dpi) is also the same — critical for working in global POS machine size and ATM machine size.

Materially, basic versions of both use durable, waterproof PVC plastic. Eco-friendly models adopt PETG (common in Europe), while premium tiers may use titanium, stainless steel, or carbon fiber.

Tiny differences are rare: some basic debit cards might skip layers (slightly thinner but unnoticeable), and premium credit cards more often use metal. In short, their look/feel are identical — only print details and financial functions differ.

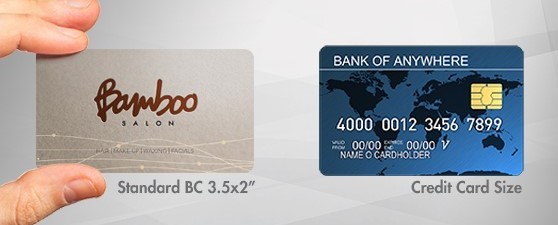

Credit Card Size vs. Business Card Size

In US, most of business card size is almost the same as credit card size.

The Evolution of Consumption Hidden in Size

Credit cards have gone from chaotic sizes to a global standard, and from paper cards to metal chip cards. We can say that the progress of consumer culture and technological development lay behind these changes, for sure.